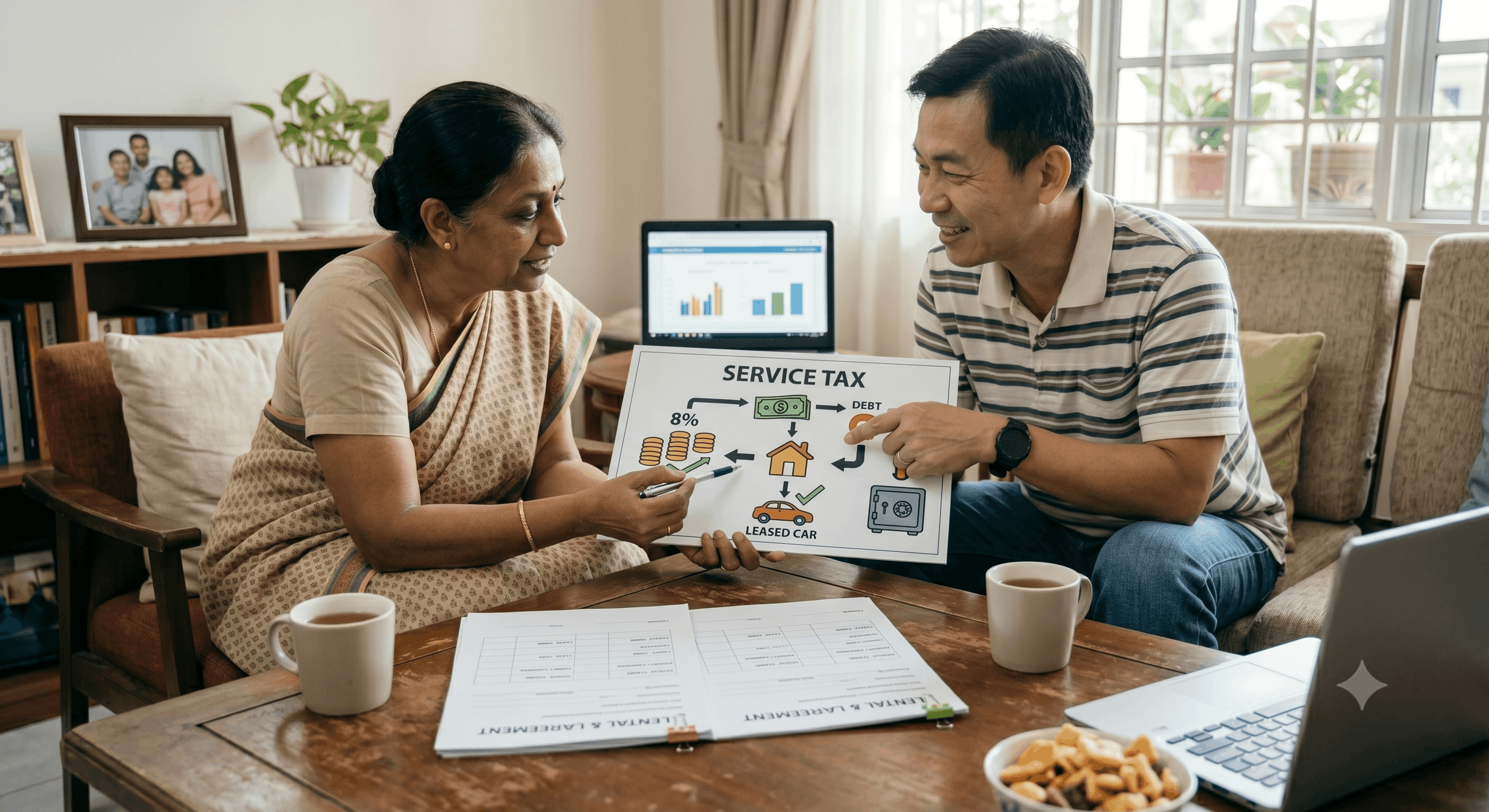

Effective 1 July 2025, rental and leasing services will be subject to an 8% service tax under Group K, First

Schedule of the Service Tax Regulations (STR) 2018. This marks a significant expansion of the service tax

regime, impacting a wide range of businesses engaged in leasing or renting tangible assets in Malaysia